Frequently Asked Questions

– Where do I start?

– What letters do I send?

– How do I write the letters?

– Who do I send them to? The creditors? The bureaus?

– What content needs to be in those letters?

– What if they just send me back a bunch of legal information and I don’t understand how to read the letter?

If you find yourself without answers to any of these questions, let us help. We have a proven method that works and we hold the creditors and bureaus responsible for reporting the right information in a timely and accurate fashion.

How do you do that you may ask?

There are 3 standards that any company who reports information to the bureaus must comply with:

1.) The information must have been reported fairly.

2.) The information must be reported accurately.

3.) The information must be substantiated in full detail.

Federal consumer laws protect all U.S. citizens against information not being in compliance with one of those 3 standards.

Personal Information

Public Records

Credit Inquiries

Account History (Collections, Charge-Offs, Late Payments, Open Accounts, Installment Accounts)

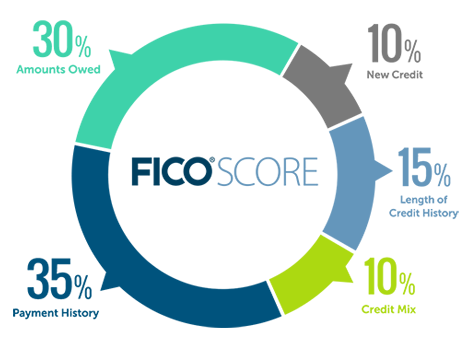

Any of these items can be disputed if they are reporting inaccurately. You have rights by the FCRA that prohibit any information reporting inaccurately to be removed from your credit file.

More questions?

Want to reach us fast? Simply click the button below and complete our email form and enter your question or message in the space provided. An email will be sent directly to our team.